Since the first OPEC oil embargo nearly a half-century ago — and more recently with Russia’s invasion of Ukraine — energy producers and consumers alike have learned important lessons about the significance of energy commodity sourcing. It all comes down to this, really: (1) know what you’ll need going forward; (2) diversify your sources of supply, focusing on suppliers who are reliable and friendly; and (3) don’t screw up by becoming overly dependent on suppliers who could prove to be sketchy. For decades, the industry’s focus was on oil and gas — which is still critical, as Europe knows all too well. But as policymakers attempt to transition to renewables and electrification, a whole new set of commodity-supply concerns is coming to the fore. In today’s RBN blog, we discuss the challenges associated with securing the key materials required to build the machinery of the energy transition.

As we said in Part 1, shifting to lower-carbon sources of energy and modes of transportation will require a lot of stuff to be mined, refined, fabricated and constructed to replace the hydrocarbon-based energy networks that run the world today. We’re talking about wind turbines, solar arrays, energy storage facilities, electric vehicles (EVs) and all of the other infrastructure and components that will need to be produced. Not only will all this stuff require staggering volumes of concrete and steel, it also will demand unprecedented quantities of metals and minerals such as copper, nickel, aluminum, lithium, chromium, and neodymium. It’s a fact that a decarbonized energy network is far more material intensive — that is, it takes a far greater investment in minerals, metals, and construction materials to produce the same energy as from hydrocarbons.

In Part 2, we looked at how the unprecedented rise in demand for key metals and minerals is already inflating commodity prices for everything, and also consequently leading to more expensive wind turbines, solar modules and batteries. How high and for how long those prices go up will depend largely on whether the policies promoting a transition to lower-carbon energy sources continue and, if so, whether the world’s miners and mineral refiners can expand production fast enough.

A key issue now is that the pursuit of materials-heavy energy infrastructure will also cause economic impacts that ripple into other markets, inflating other costs where the same minerals are needed to build computers, manufacturing equipment, housing, and all manner of everyday consumer products. Just as inflated prices for crude oil and natural gas rip through the economy, so too higher costs for basic minerals. And while materials have for most of recent history constituted only a minor share of the final cost of most products and services, that share becomes major and inflationary if mineral and metal prices balloon. And prices will continue to escalate if demand growth continues to outpace supply.

That demand for metals and minerals could soar far beyond current levels for a simple reason: the fact is that, despite headlines about the rise of renewables and EVs, wind turbines and solar modules combined now supply only a few percent of total global energy, and batteries still power less than 1% of all on-road vehicles. Expanding those shares by the leaps and bounds imagined in the next decade or two will necessarily entail enormous minerals demands.

As we noted in earlier episodes in this blog series, the physical realities of renewables and batteries vs. hydrocarbon-based energy means there will need to be a roughly 1,000% increase in the use of key minerals to replace the same energy supplied by gasoline, diesel, natural gas, propane, etc. Consider, for example, that about 400 pounds more aluminum and 150 pounds more copper are used to build an EV compared to a standard car powered by an internal combustion engine. Multiply that millions — and then tens of millions — of EVs a year and then add in the booming demand for those and other minerals needed to build more wind and solar machines and the volumes required are daunting. In fact, a recent minerals analysis from banking giant ING found that the International Energy Agency’s (IEA) energy transition goals would consume about half of all current aluminum and copper production and about 80% of global nickel output.

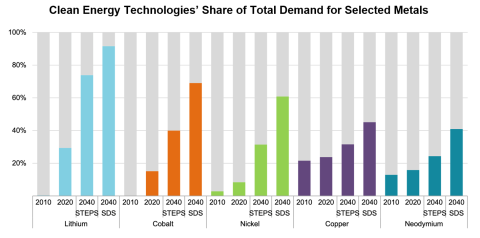

The challenge in meeting energy transition mineral demands and the potential for long-term systemic inflation is perhaps best illustrated by this: The IEA expects that the pursuit of climate-friendly policies on renewables and electrification will make the energy sector — which now accounts for only a minor share of the total use of key minerals — by far the dominant user of many key metals and minerals, eclipsing uses for all other purposes. For example, the energy sector currently uses less than 10% of all the nickel produced (second green bar in Figure 1), but if transition goals are to be achieved, that would rise to 40% under the IEA’s Stated Policies Scenario (STEPS; third green bar), which is based on what governments already have committed to do regarding climate change, and 60% under the agency’s Sustainable Development Scenario (SDS; fourth green bar), which is based on what would need to be done to achieve the goals of the Paris Agreement. There also would be similar steep increases in the energy sector’s share of using lithium, cobalt, copper, and neodymium.

Figure 1. Clean Energy Technologies’ Share of Total Demand for Selected Metals. Source: IEA

The IEA also has concluded that today’s global mining capabilities, including plans for expansion, cannot come close to producing the quantities needed. So, it shouldn’t be surprising that lithium prices, for example, have soared nearly 1,000% in the past two years, or that there’s been over 200% inflation in copper, nickel and aluminum, with the last of these now at a 30-year high. With governments proposing to double down on energy-transition policies, demand will accelerate even more beyond supply. That is an incendiary formula for far more minerals inflation.

[RBN Energy’s U.S. CO₂ Infrastructure map brings together legacy Enhanced Oil Recovery (EOR) assets, as well as announced large-scale Carbon Capture and Sequestration (CCS) and Carbon Capture, Utilization and Sequestration (CCUS) projects, all in our signature concise, accurate, and intelligible style. Click here for more information.]

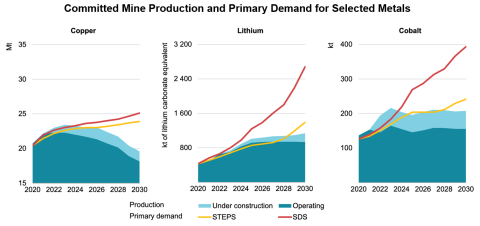

Figure 2 shows the capacity of operating mines (dark-teal layer) and mines under construction (light-teal layer) for three key metals — copper, lithium and cobalt — as well as forecast demand for the metals under the IEA’s STEPS and SDS scenarios. As you can see, the gap between capacity and demand for each of the metals widens considerably through the second half of the 2020s — a worrisome trend. The long lead times required for developing new mines — and the fact that plans are not already underway to build the necessary production capacity — should be raising red flags for those who believe the materials will be available to build the machinery of the transition. And it should worry economists and policymakers regarding the systemic impacts on inflation.

Figure 2. Committed Mine Production and Primary Demand for Selected Metals. Source: IEA

Late last year, International Monetary Fund (IMF) economists published an analysis of the mineral commodity implications of the IEA’s energy transition plan. They concluded that metal prices would reach historical peaks “for an unprecedented, sustained period of roughly a decade.” That inflation would be bad enough under normal circumstances, but with metals and minerals playing outsized, high-volume roles in the energy transition, the impact is compounded. For example, a recent U.S. Geological Survey (USGS) paper pointed out that doubling aluminum prices would increase heavy vehicle production costs enough to wipe out the entire profit margin for U.S. manufacturers. Companies would, of course, have to hike vehicle prices to recoup the higher costs.

The potential for systemic, long-term metal and mineral inflation would be something new for today’s policymakers. The entire 20th century was a period of slow decline in average minerals prices. But that trend began to reverse about a decade ago, especially for aluminum, nickel and copper. Whether the world returns to the comforts of long-run cost declines, or to more inflation, will now be dominated by energy policies driving mineral supply shortages. And it will also be determined — in no small irony — by policies that increase the cost of hydrocarbons since those fuels are critical to global mining. Oil and gas account for about two-thirds of the overall mining sector’s energy use; the rest is electricity, which in many parts of the world is produced primarily by burning hydrocarbons. Overall, spending on energy can account for up to 40% of total costs in the mining ecosystems.

Supplying the necessary minerals will require opening more mines — lots of them — and building more mineral processing facilities as well. As with petroleum, the raw product must be refined at big chemical plants that consume lots of energy. But the global average time from qualifying a property to bringing a new mine into operation is 16 years (once more, per the IEA). With dozens upon dozens of new mines needed, each at the scale of some of the biggest mines in the world today — and each requiring tens of billions of dollars of capital — it remains to be seen if that happens. So far, it has not.

Beyond economics, there are also environmental and geopolitical challenges — both of which also entail economic consequences — arising from realignments of energy material supply chains. For example, the U.S. today is dependent on imports for 100% of some 17 critical metals and minerals and, for 28 others, net imports account for more than half of existing domestic demand.

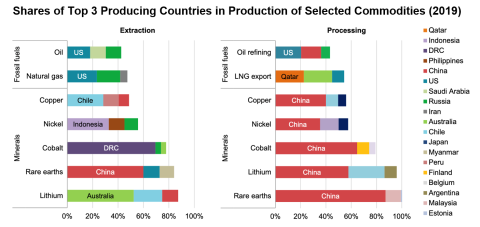

Figure 3 shows the shares of global extraction and processing of key energy-related commodities (oil, natural gas, copper, nickel, cobalt, etc.) held by the three leading producers for each commodity (tri-colored bars). In a few cases, the top producers of key minerals include countries friendly to the U.S. –– Australia, the leading producer of lithium, certainly would qualify. But the rest of the story isn’t so heartening. Russia — now a pariah state to the U.S. and its allies — is one of the world’s top copper producers, accounting for 4% of global supply (roughly co-equal to the U.S.) and also produces about 6% of the world’s aluminum (4x the U.S. output) and 10% of its nickel production (#3 in the world). Then there’s Chile, the world’s biggest copper producer, which, while it has had good relations with the U.S. in recent years, now has a socialist president who has promised to tighten the environmental regulations governing mining, which could affect future production there. (The #2 and #3 copper producers are Peru and the Democratic Republic of the Congo.) The top nickel producer is Indonesia, which is not generally viewed as having a stable political environment. Then there’s China. Not only is China the top aluminum producer, for example, with a 40% market share, but it has a market dominance in what the IEA calls “energy transition minerals” that is double OPEC’s share of oil markets.

Figure 3. Shares of Top 3 Producing Countries in Production of Selected Commodities (2019). Source: IEA

Of course, there also are environmental implications associated with the need for many more mines and processing facilities to meet the demand for energy-transition metals and minerals. Producing a pound of many key materials often requires the extraction and processing of many tons of rock and dirt, and many mines are sited in remote, previously pristine areas. Finally, there’s the matter of whether we want to be securing the materials for our energy future from countries that lack even the basic labor and safety protections we take for granted in the U.S. and Canada.

In the next and last installment in this series, we will explore the challenges and opportunities associated with a radical expansion of the mining ecosystem.

Mark P. Mills is a senior fellow at the Manhattan Institute; a partner in Cottonwood Venture Partners, an energy-tech venture fund.